How to Use XGBoost for Time Series Forecasting

Last Updated on August 27, 2020

XGBoost is an efficient implementation of gradient boosting for classification and regression problems.

It is both fast and efficient, performing well, if not the best, on a wide range of predictive modeling tasks and is a favorite among data science competition winners, such as those on Kaggle.

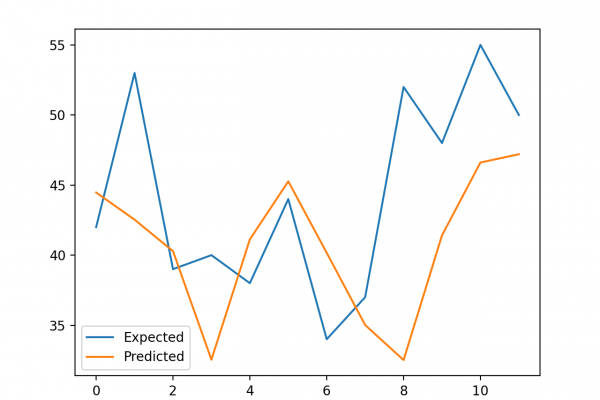

XGBoost can also be used for time series forecasting, although it requires that the time series dataset be transformed into a supervised learning problem first. It also requires the use of a specialized technique for evaluating the model called walk-forward validation, as evaluating the model using k-fold cross validation would result in optimistically biased results.

In this tutorial, you will discover how to develop an XGBoost model for time series forecasting.

After completing this tutorial, you will know:

- XGBoost is an implementation of the gradient boosting ensemble algorithm for classification and regression.

- Time series datasets can be transformed into supervised learning using a sliding-window representation.

- How to fit, evaluate, and make predictions with an XGBoost model for time series forecasting.

Kick-start your project with my new book XGBoost With Python, including step-by-step tutorials and the Python source code files for all examples.