How to Develop Multilayer Perceptron Models for Time Series Forecasting

Last Updated on August 28, 2020

Multilayer Perceptrons, or MLPs for short, can be applied to time series forecasting.

A challenge with using MLPs for time series forecasting is in the preparation of the data. Specifically, lag observations must be flattened into feature vectors.

In this tutorial, you will discover how to develop a suite of MLP models for a range of standard time series forecasting problems.

The objective of this tutorial is to provide standalone examples of each model on each type of time series problem as a template that you can copy and adapt for your specific time series forecasting problem.

In this tutorial, you will discover how to develop a suite of Multilayer Perceptron models for a range of standard time series forecasting problems.

After completing this tutorial, you will know:

- How to develop MLP models for univariate time series forecasting.

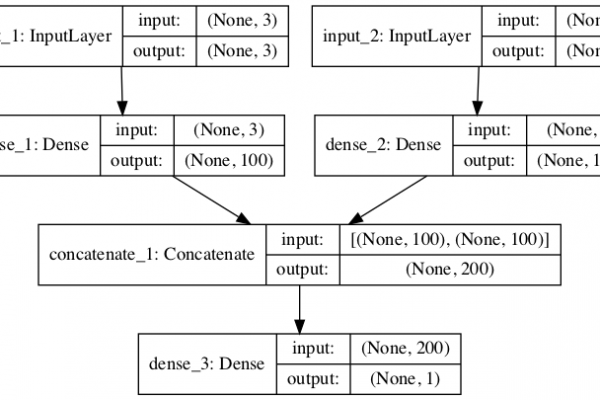

- How to develop MLP models for multivariate time series forecasting.

- How to develop MLP models for multi-step time series forecasting.

Kick-start your project with my new book Deep Learning for Time Series Forecasting, including step-by-step tutorials and the Python source code files for all examples.

Let’s get started.